No matter where you are in life, it’s critical that you start saving for your future! But in order to save you have to make a plan. Print and use the budget tracker below to track your income and expenses each month!

For a step by step guide on how to use the tracker, scroll down.

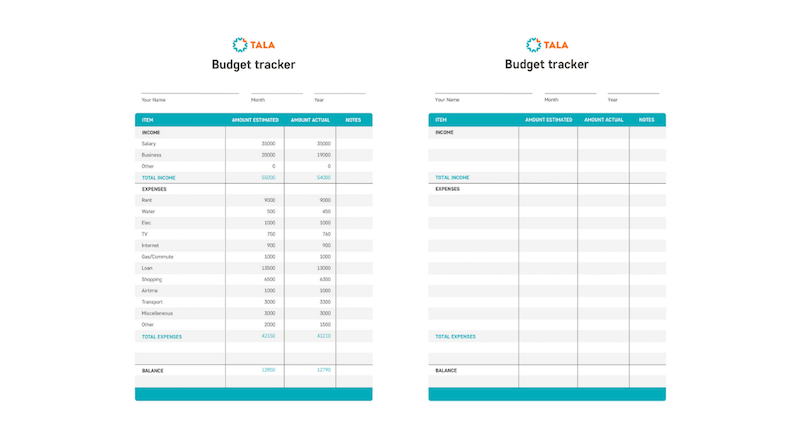

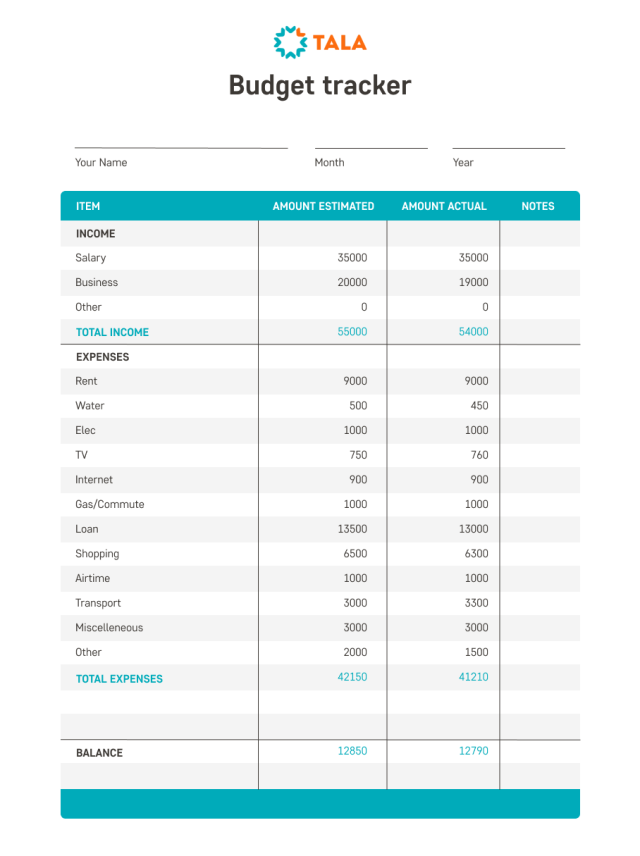

Example

Steps to use the tracker

At the beginning of each month:

1: Determine your income.

At the top of the budget tracker under “Amount Estimated”, write down the money you get from all sources: your salary, money from side hustles, business income or income from investments. Leave the “Amount Actual” column empty for now.

2: Determine your monthly expenses.

Below your income, write out all of your expenses — expenses are everything that you will spend money on each month. Again, leave the “Amount Actual” column empty for now.

3: Determine your balance.

This is the step where you will determine how much you are able to save or how much you are overspending each month.

First, take your total income and subtract your total spending. (Income – expenses = balance)

To use the example above, if you make KSh 55,000 and you think you will spend KSh 42,150, that will leave you with a balance of KSh 12,850 at the end of the month.

- KSh 55,000 (income) – KSh 42,150 (expenses) = KSh 12,850 (balance)

In other words, you will spend KSh 12,850 less than you make. That is all money you can put towards savings! If you keep that up each month you could save KSh 154,200 in just one year.

4. Review and adjust your budget.

Remember the column on the left (Amount Estimated) is only an estimate at the beginning of the month. Now it’s important to review what your actual expenses were to see if you were able to reach your savings goal or if you need to adjust your budget.

So, at the end of the month, go back and write down what all of your expenses actually were under the “Amount Actual”. Then revise your budget for the next month accordingly.

In the example above, you can see that the actual income was slightly smaller than the estimate and the expenses were slightly higher. Therefore, they can determine that they will need to reduce some expenses to achieve the savings goal they had set with the previous month.