Have you ever applied for a loan with a financial institution but it was not approved? If the answer is yes, this may be due to various factors, although we can summarize it in two main reasons:

- You have no credit history

- You have a report in the CRB (Credit Reference Bureau) with a negative rating

In this article, we are going to focus on the second option – when there is a negative report in the Credit Reference Bureau.

Let’s start by clarifying that being in the Credit Reference Bureau (CRB) is not necessarily good or bad. Records are entered into the CRB anytime a person obtains a credit or loan or issues a dishonoured cheque. These records can have a positive or a negative rating.

It is important to get rid of the mistaken belief that being reported in the Credit Reference Bureau (CRB) is a black list where people who do not pay or have a debt are found.

It is a report that financial institutions use to evaluate or underwrite credit applications and decide whether to give credit or not, and this will depend on your credit score, that is, if you have a good or bad rating.

Therefore, saying that we want to leave the Credit Reference Bureau (CRB) is not the most appropriate direction, because we would only leave if we stop acquiring financial services and when we have no credit transactions.

What we can do is improve our credit behaviour to obtain a higher score. At Tala we share 5 steps that will help you “get out of the Credit Reference Bureau (CRB)”, or rather, to have a positive rating.

- Check your credit bureau report.

Credit entities such as the Metropol Credit Reference Bureau or TransUnion Credit Reference Bureau Kenya are private and do not belong to any banking or government institution, so if we require their services they will have a cost.

This report will show the behaviour of each of your accounts; active, closed and current accounts. There are those accounts that are 1 to 89 days past due, those that are more than 90 days past due, and finally bad debts.

If you want to know your Tala outstanding loan balance, dial USSD *846# or send a message to 21991 with your Tala registered phone number or inbox us on Twitter/Facebook or email to hello@ke-support.tala.co - Get up to date with your debts.

Once you know that the financial institutions have reported you, and how much you owe, do not wait any longer, create a strategy and start paying, it may sound quite obvious, but it is crucial and there is no other way if you want to “leave the CRB” and recover a good history with a good score you need to catch up and settle all your debts. - Negotiate with financial institutions and seek to restructure your debt.

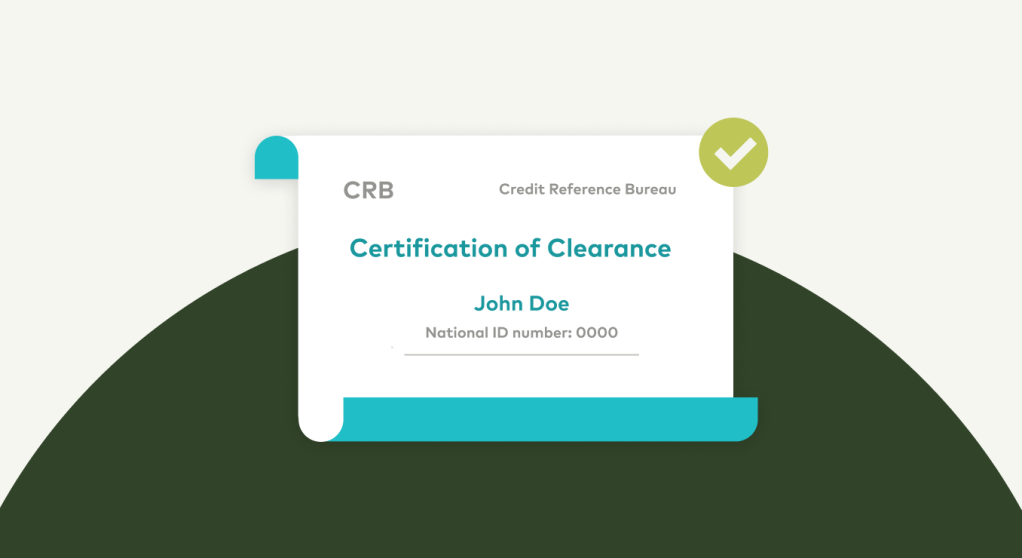

Having the best intention to settle our debts is of the utmost importance, although it will not always be enough, maybe because the interest is excessive and your level of debt has increased. Approach directly with the institutions and propose a restructuring of your debt, a payment plan with a different interest rate that allows you to pay constantly. - Request your clearance certificate/letter.

When you settle your debt, request the clearance letter at each CRB. This letter certifies that a certain natural person has settled his debt, the date on which the payment was issued, the amount paid, and the business name of the financial institution to which it has been settled.

Having this letter will be useful when you want to verify that you are free of debts, and it will facilitate the clarification process.

If you currently have a debt with Tala and want to change your CRB score, do not hesitate to contact us! Remember that we do not charge daily interest on your delayed loan, and we do not seek to make it difficult to settle your debt, on the contrary, our advisors will seek the best alternative that suits your possibilities.

We invite you to continue learning about financial education at our learning center on this website and the Tala app.